Is a perverted definition of capital efficiency fuelling unemployment?

One of my favourite economic thinkers is the 19th century French satirist, Frederic Bastiat. And among my favourite sketches of economic absurdities are those dealing with the sophisticated thoughts of Robinson Crusoe and the profound simple logic of his servant Friday.

One such has Crusoe toiling for days on shaping a single board from a tree to construct his home on the island. One day he walks on a beach to discover a perfectly shaped board that has washed ashore from a shipwreck. His delight at being able to save much work is quickly dispelled when he realises that if he uses the board he will be doing himself out of work. So he turfs the board back into the sea.

I had a similar experience when at a mine consulting site there was talk of imminent retrenchments among the surface cleaners. When their co-workers got wind of it, they set about overturning trash bins and strewing the contents about to ensure that their colleagues would remain needed. The mine management’s response was swift in employing motorised sweepers and retrenching a large number of them.

Whenever one raises the question whether technology is contributing to unemployment, there is a knee jerk dismissive response, the most disdainful of which is that it implies resistance to progress and a denial of all the good things that technology has brought us. That clearly is not the issue, but ignoring the fall out of technology is like trying to ignore that certain drugs have side effects that have to be managed. Similarly, the effect of technology on climate change is today widely acknowledged and being addressed – some would argue not seriously enough.

But greater resistance to the question comes from conventional economics, rooted in a very long held belief that far from destroying jobs, technology in all its forms actually creates more jobs. It has been argued for as long as I can remember that workers displaced by technology would find employment “elsewhere”, albeit after obtaining new skills and additional training. That “elsewhere” or “what” is seldom defined, let alone quantified. Even vaguer is how that can effectively be achieved. But the assumption that technology on balance creates more jobs is in itself false.

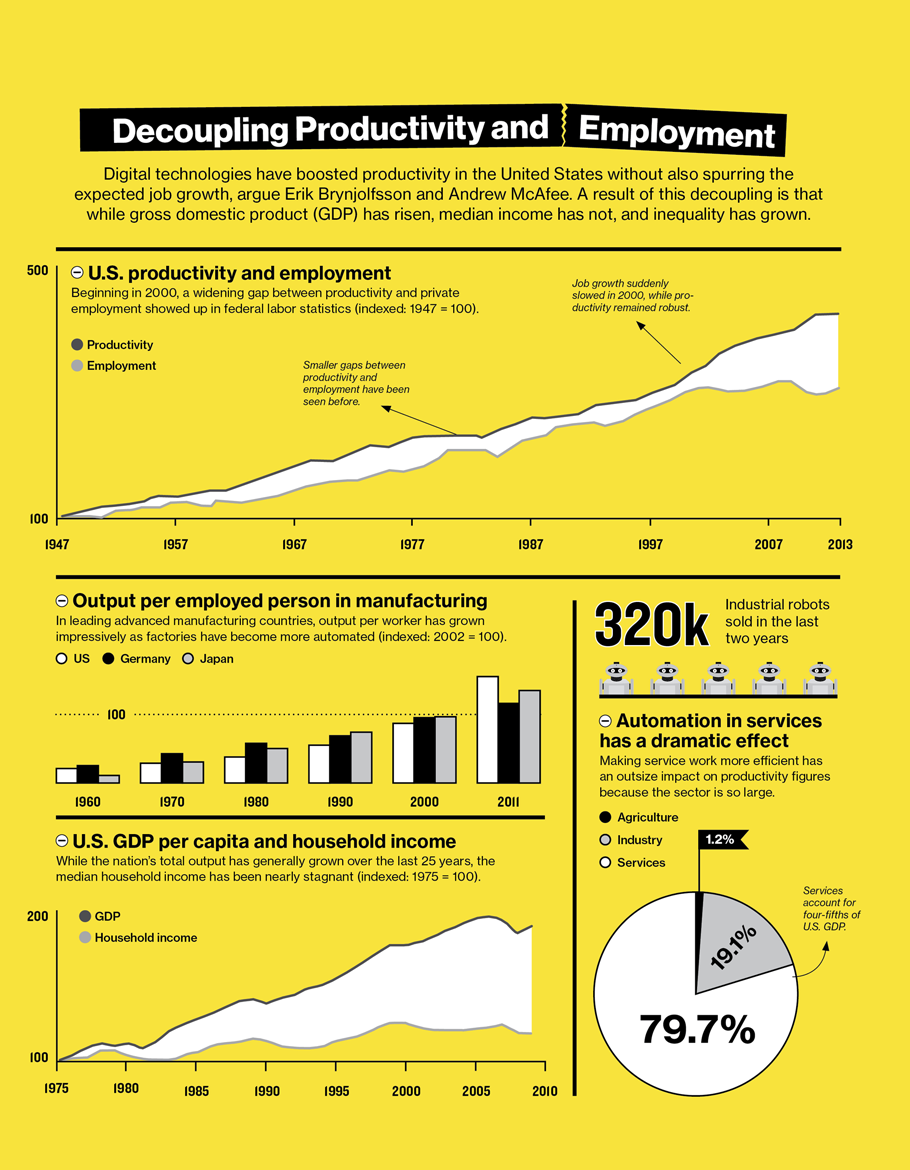

Research by the world leading Massachusetts Institute of Technology (see graph here) provocatively suggests that the opposite could be true, pointing to a growing disconnect between productivity and employment. Productivity gains have outpaced employment since the late 1950’s becoming quite pronounced since 2000. While others in the fuller report (see here) have their doubts about technology on balance actually destroying jobs, the theory that it automatically increases employment simply no longer holds true.

{kind=link}

Which may explain increasing public insecurity about the pace of innovation. More than half of the respondents to the latest Edelman survey said they distrusted the speed of development in technology. So if technology is our friend, which undoubtedly it is, why is it also perceived to be a threat? An answer most likely lies in not seeing technology in isolation, but in the broader context of the obsession with the holy grail of capital efficiency, which is the conventional understanding of improved productivity. Bear in mind that the basic measurement of capital efficiency is return on investment. Technology is one element of this. The others are maximum returns on capital in the shortest possible time (or profit maximisation and shareholder value criteria); and investment for maximum short term yields. They are all linked.

Ironically, capital efficiency, especially in the short term, and its main tool of profit maximisation is not always technology’s friend. Technology has two steps – discovery, which is finding or developing a new and creative idea; and innovation, which is putting that idea into practical use. It is often very difficult to find capital supporting untested and new ideas. Even in innovation, the focus on profit maximisation could impede research and development. Developing longer term technology improvements could be stilted by the requirement for higher immediate returns on capital. The latter also specifically targets the involvement of labour as a cost. Clearly the behaviour of labour itself can contribute to that momentum.

It is indeed possible to use technology to improve profits without necessarily increasing wealth creation itself. Simply displacing labour will do that. But the perceived threat of technology to jobs will be reduced when it is seen for the most part as being in the interest of customers and the broader public and not simply to maximise profit.

The third part of capital efficiency, that of investment, has perhaps a less tangible link to technology per se, but in ensuring maximum returns in the shortest possible time, it adds to the general milieu of distrust, unemployment, and income inequalities. This is the diversion of money into highly speculative financial markets and the growing asset bubbles in stocks, bonds and property. In the end there is less motive to invest in people and more in assets.

Capital efficiency is the cornerstone of Western economic thought. This is at least partly due to a lingering perception that profits are equal to value added or wealth created, or even that it is the primary enabler of wealth creation and therefore the most important component of GDP. To challenge its paramountcy borders on economic heresy and most mainstream economists will not go much further than calling for some constraint in its pursuit – if that. I must concede that my definition of capital efficiency may differ from the conventional which relates narrowly to production and not more broadly to organisational deployment such as share buy-backs; mergers and acquisitions; reserve hoarding and investment in flighty global capital movements.

So to be clear, capital efficiency is an excellent tool in ensuring best use of resources. But it is not the only one. Indeed, value-added or wealth created is superior to the narrow capital efficiency focus which should never be an exclusive and paramount purpose. That’s very much like putting an athlete on steroids.

Returns on capital go to the owners of capital, a relatively small section of the population, apart from the highly diluted individual holdings in pension and other investment funds. Ultimately there must be a backlash. If Oxfam is correct in its calculation that soon only 1% of the people in the world will own more than half of global wealth, at least partly attributable to the emphasis on capital efficiency, it poses a real threat to the global economic machine.

It means simply that half of the world’s wealth is mostly trapped in an asset bubble, never to spread in consumption expenditure, that translates into demand and that is the real fuel of production. In short, the more machines and technology replace people, the more tenuous the link between production and consumption, and the weaker demand, simply because fewer people can afford to spend.

Even if we had to overcome that in future decades through some fancy fiscal footwork in redistribution, humanity will confront something most old folks quickly get to know. The two primary challenges in life are provision and purpose.

Without employment, most people will simply lose purpose, perhaps the more important of the two.

Yeah It's good I appreciate this article. I recommand it to my friends,I,ll be back here again and again . Visit our blog for more .

ReplyDelete1. What determines the software price? Is it Per Seat or Per User or Per Processor? The cost of software is determined in many ways. The two most popular ways are Per Seat or Per Concurrent User. P... Source

ReplyDeleteThere are three vital components that govern operations inside a plant or inside a software unit. They are People, Process and Technology. One cannot exist without the other. This article describes the three building blocks and the interaction between these building blocks. phone tracker

ReplyDeleteOne can think of several metaphorical comparisons to describe software development, such as writing a book or building a house. Some of them are a good light in the dark, some are rather misleading. route planning software

ReplyDeleteThis question has been in the minds of most folks. In the midst of the uprising technology advances we are also faced with lots of negative effects we see today. This question is actually related with life and medicine as technology has solved a lot of our health problems in the past that was almost impossible to deal with. Marceline

ReplyDeleteWhat is the best choice for the company who can't find a single software solution that addresses all its needs? Bespoke application development can become the way out of the situation when available products don't fit companies need for any reasons. Let's explore the bespoke software advantages and disadvantages and see if it worth for enterprises to step into this area. BYJU’s App For PC

ReplyDeleteTechnology & HR-Leverage one for the other: "Technology and HR are enablers of business. Integration of the two would mean not only harmonious co-existence but also leveraging one for the other. Leveraging of technology for HR would mean digitizing the mundane HR activities and automating the back office and transactional activities related to recruitment, performance management, career planning, and succession planning, training and knowledge management. Leveraging HR for technology implies managing change associated with technology by way of communication, training, hiring, retraining, stakeholder analysis and conscious keeping. Thus they can play complementary roles." best xmind competitor

ReplyDeleteYour writing has a calming effect on me. It's like taking a virtual retreat every time I read your blog. Buy remote work tracking software from remote work tracking software

ReplyDelete